The AI Gold Rush in Financial Services and Why Most Won’t Strike It Rich

The AI revolution in finance is real, but venture returns may not be.

Yes, GenAI is moving from demos to decisions in financial services. What began as lightweight copilots for summarization and information retrieval has rapidly evolved into embedded infrastructure for how banks and investors source deals, diligence risk, execute transactions, and manage portfolios.

The opportunity is clear: investment workflows are one of the largest knowledge work markets globally with roughly 1.5 million professionals representing an estimated $225–525 billion in annual labour spend. These workflows are data-dense and repetitive making them a natural target for AI-driven productivity gains.

While the market opportunity is undeniable, we believe the scope for venture-scale outcomes within AI-native workflow platforms for financial services is more limited. AI will meaningfully reshape how work gets done across banking and investment workflows, but the question of what providers will power these workflows and where value will accrue remain unknown.

At the application layer, we believe commoditizing model capabilities and structural barriers to adoption will limit the number of durable winners. Ultimately, we believe the majority of value will accrue to horizontal platforms that sit upstream of specific use cases and can scale distribution without the customisation bottleneck of vertical point solutions. The exception will institution-specific deployments built by forward-deployed teams, a model that increasingly resembles a consulting business wrapped in software – though their ultimate scale is likely constrained by the economics of a services business.

Financial Services Is Finally Ready for AI

Investment workflows have resisted automation for years. There are many structural reasons - fragmented data, complex judgment-based processes, and strict requirements around explainability and auditability – but it ultimately comes down to trust. Historically, users did not trust the fidelity of automated outputs. There were two facets to this problem - AI lacked the necessary capabilities to provide and execute trusted outputs, and institutions were not equipped to implement AI at an institutional level.

This is now changing: technology has matured, and economic pressure within financial services is rising, making front-office workflows ripe for disruption.

Technology is ready to scale:

- Synthesis at scale. Modern models can synthesize thousands of pages of filings, transcripts, and reports with increasing accuracy.

- Verifiable outputs. Improvements in retrieval and traceability allow outputs to be cited and verified which is critical for regulated environments.

- Agentic execution. Agentic workflows can now execute multi-step processes, from monitoring companies to updating research and generating reports.

- Enterprise-ready infrastructure. Enterprise-grade infrastructure and institutional governance have caught up, enabling AI to be deployed securely, compliantly, and at scale within financial institutions.

Industry is under pressure:

- Cost pressure. Banks and asset managers are facing sustained pressure on cost structures and are actively seeking ways to increase capacity without adding headcount.

- Untapped proprietary data. Financial institutions sit on vast amounts of trading histories, client interactions and internal research that has historically been siloed. AI now makes it possible to operationalize all of this data at scale.

- Macro headwinds. Fee compression, deal slowdowns and headcount pressure are sharpening the ROI for AI – and lowering internal resistance to replacing analyst hours with automated workflows.

Companies are ready to implement, but are users ready to adopt? Companies are experimenting with different providers, but adoption tells a different story. Across our network, we consistently hear of low usage rates, high churn, and an inability to track whether tools are being used at all – a least for vertical-specific platforms. These issues are not unique to financial services – whisperings across the industry suggest other “early vertical winners” in services industries such as legal are also seeing churn.

The outstanding question is whether incumbent service providers successfully incorporate AI – whether built in-house or via acquisition – or do you need to build AI-native firms from the ground up? The even larger question looming over both: will foundation models commoditise the application layer before any of these players establish durable footholds?

Our Framework for Evaluating AI for Front-Office Workflows

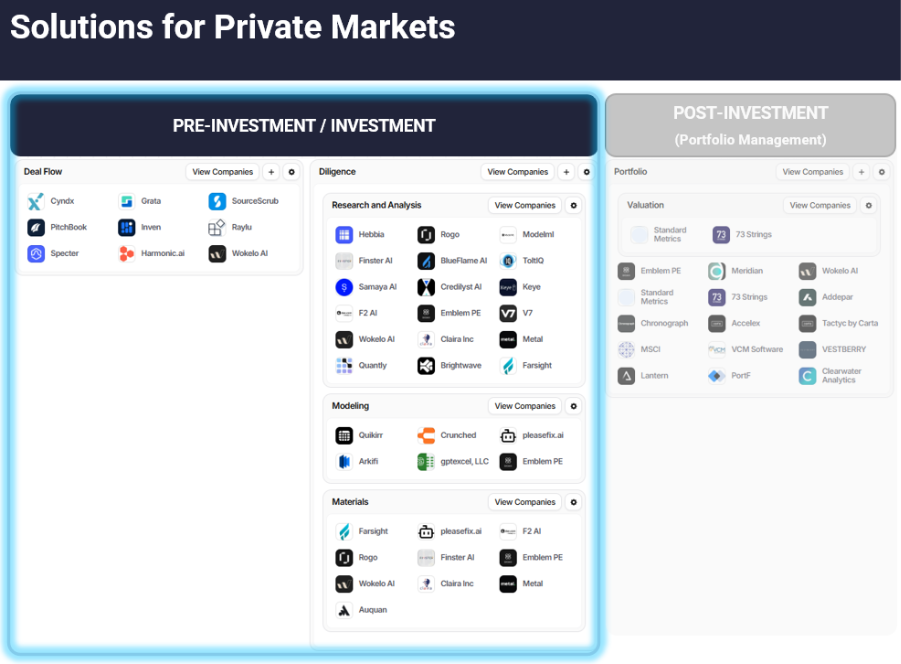

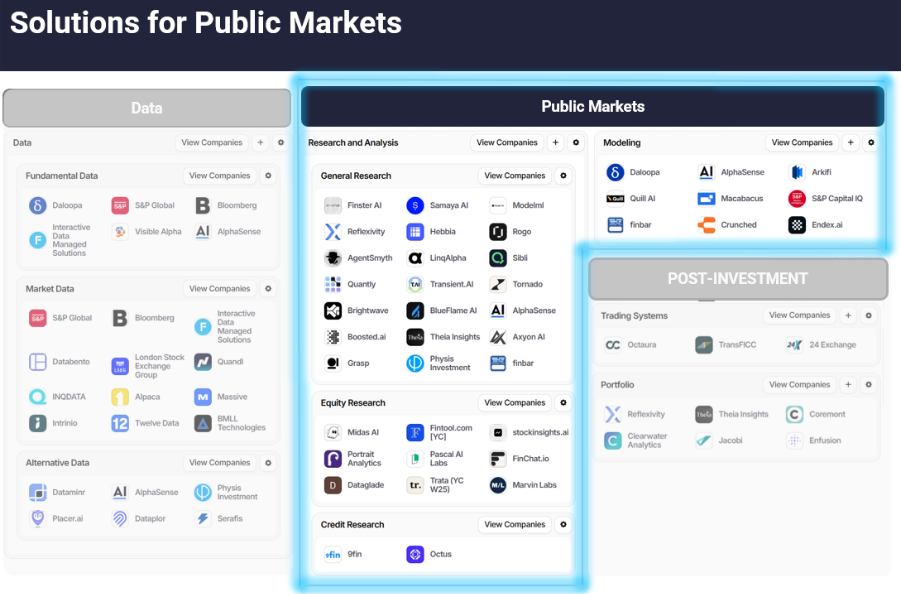

We assessed AI applications across front-office banking and investment workflows from pre-deal/investment (sourcing, research, analysis) to execution (material creation, decision-making, execution) and post-investment workflows (portfolio monitoring). We also looked at the systems of record and data infrastructure underpinning these workflows.

We are starting at the beginning of the taxonomy since we see pre-investment workflows as a natural beachhead. These workflows rely heavily on unstructured data, involve repetitive but high-value tasks, and offer immediate ROI from time savings. Summarizing a data room, extracting key metrics from filings, or preparing a first-look investment memo can save hours of analyst time without introducing significant regulatory risk.

A multitude of solutions have emerged in this space from early leaders (Hebbia) to the latest wave of high-profile entrants (including Rogo and Model ML) that are drawing considerable investor interest despite limited evidence of sustained adoption. However, we’ve found POCs and even signed enterprise contracts do not necessarily correlate with adoption.

There is a lot of noise, but is there any real adoption today?

Much of the front office is theoretically automatable today—but in practice, doing so requires heavy customization through forward-deployed engineering, limiting scalability and concentrating adoption among the largest institutions. As a result, innovation has focused on a narrow set of use cases:

- Initial company research and ramp-up

- Search and synthesis across filings, transcripts, and internal documents

- Summarization and meeting preparation

- Data extraction and population of historical models

These tools share three defining characteristics:

- Offer clear and immediate time savings;

- Layer on top of existing workflows rather than requiring wholesale change; and

- Demand minimal behavioural adjustment from front-office workers.

However, structural constraints particularly acute within financial services have slowed adoption:

- Trust and accuracy are non-negotiable. Even small errors undermine credibility since outputs need to be fully auditable and near perfect. In practice, this often leads analysts to double-check AI outputs – eroding productivity gains.

- Workflow inertia is real. Investment processes are deeply ingrained and idiosyncratic. Changing tools requires behavioural shifts, not just technical integration, and analysts are often reluctant to abandon established workflows.

- Data access matters more than model capabilities. As public data becomes commoditized, differentiated insights depend on proprietary sources – expert calls, internal data and research – which many AI tools cannot access.

- Human judgment remains central. AI accelerates analysis but still falls short on causality, context and decision-making – leaving humans firmly in the loop for real-world investment decisions.

We are seeing domain-specific players within financial services expand beyond these initial use cases as capabilities commoditize, but even in less crowded areas it is unclear whether these companies can build sustainable moats. Differentiation depends on deep integrations and proprietary data – which often requires forward-deployed engineering and bespoke builds. The need for customisation today means it will be harder to scale quickly, and solutions may prove effective within a single institution, but face real friction replicating that success at speed across the market.

Analysts are deeply embedded in Excel, PowerPoint, and internal systems and reluctant to adopt tools that disrupt established workflows. As a result, AI is emerging as a productivity layer, not a replacement for human judgment. Across both buy- and sell-side workflows, the dominant model is augmentation with human oversight, not end-to-end automation.

The real question – is automating existing workflows, user tools and co-pilots, the end state? We do not think so. We expect workflows to be reimagined over the next 5 to 10 years, rendering the current crop of Microsoft Excel and PowerPoint copilots currently being deployed on both the buy-side and the sell-side obsolete in the medium-to-long term.

Where Will Value Accrue?

This brings us back to the core question: where will value accrue as front-office workflows are automated? To answer this, we assessed defensibility across each stage of the workflow.

High Defensibility: Data and Systems of Record. The most defensible opportunities are anchored in proprietary data and deeply embedded workflows. Portfolio monitoring systems exemplify this—sitting at the core of fund operations, tightly integrated with internal data, and characterized by high switching costs. Similarly, platforms that unlock and operationalize proprietary data sources benefit from durable advantages.

Medium Defensibility: Workflow Augmentation. Tools that enhance modelling, CRM, and other high-frequency workflows offer moderate defensibility near-term – driving clear near-term productivity gains by embedding in workflows but remaining vulnerable longer-term. Still, early integration can create medium-term defensibility as we’ve seen with prior vertical-specific tools that have become industry standard such as Bloomberg for traders and CoStar for real estate investors.

Low Defensibility: Edge-of-Workflow Tools. Sourcing, research summarization, and generic copilots are the least defensible solutions. As foundational models absorb these capabilities and push into financial workflows, many startups risk becoming thin wrappers around commoditized functionality – a concern widely echoed by market participants. “Commoditized” here means that capabilities which once required significant proprietary engineering – parsing a data room, extracting key metrics from filings, summarising earnings calls – can now be replicated quickly and cheaply by any team with access to a foundation model API, with no meaningful technical barrier to entry.

Taken together, commoditizing model capabilities, weak defensibility across most categories, and persistent adoption barriers will limit the number of durable winners at the application layer. As such, we believe the majority of value will accrue to horizontal platforms that, unlike vertical point solutions, can amortise the heavy costs of enterprise compliance, security, and workflow integration across a broad user base, scale distribution without proportionally scaling cost, and capture value regardless of which specific workflows ultimately automate. The exception is institution-specific deployments built by forward-deployed teams — a model that increasingly resembles a consulting business wrapped in software, though growth will likely be linear rather than exponential.

How Is AI Being Deployed in Financial Services?

In practice, most institutions are adopting a hybrid approach, but we are seeing four primary models for integrating AI today:

- Direct use of foundational models

- Vertical AI startups (third-party applications)

- Embedded AI within existing financial software

- In-house enterprise builds

While large firms are investing heavily in internal capabilities, building robust AI systems requires significant talent and resources. In our conversations, many institutions outside the top tier initially set out to build in-house but ultimately pivoted to third-party solutions. As a result, we believe most institutions will continue to rely on external providers, particularly for non-core workflows. However, this does not guarantee success for verticalizsed solutions.

Integration challenges remain significant, and internal tools, while often less sophisticated, benefit from direct access to proprietary data and workflows. At the same time, incumbents are rapidly embedding AI into their existing platforms, leveraging distribution and customer relationships. The result is a competitive landscape where differentiation is difficult and consolidation is likely.

Which new entrants are worth watching?

Investing ultimately comes down to one question – where will we generate the highest risk-adjusted returns? While investors assess different opportunities with different risk profiles across asset classes, similarities have led many start-ups to sell to both the buy-side and sell-side across asset classes. However, differences in workflows and data availability have led to some more niche solutions emerging, and we are seeing different market segments adopting faster. For example, while private market investors have been relatively early adopters, public market investors have remained more cautious.

For institutions evaluating third-party vendors, we favour providers that combine technological capabilities with domain expertise. While a number of these companies rely on forward-deployed engineers, they do offer durability. However, adoption is still the key challenge as most solutions are sold through C-suite relationships, but signed contracts do not necessarily translate into usage. Without sustained adoption, long-term staying power of third-party vendors remains uncertain.

Where Is the Market Going?

Over the next 12–18 months, we expect the market to transition from experimentation to more embedded use cases. Adoption will concentrate around solutions that combine three elements:

- Deep workflow integration

- Access to proprietary data

- Institutional-grade governance and compliance

At the same time, generic, wrapper-style tools will face increasing commoditization.

As functionality converges and foundation models continue to improve, differentiation will become harder to sustain. Market consolidation is likely, with incumbents acquiring promising startups to maintain relevance. Within this universe, we think vendors that have combined deep AI expertise with deep knowledge of the financial services industry will have the best chances of succeeding. As someone put it – your average banking exec doesn’t want to buy from some guy in his 20s in a hoodie.

In Conclusion: A Large Market with Concentrated Outcomes

AI will undoubtedly reshape banking and investment workflows. The opportunity is real: a large, high-value market with clear productivity gains and strong demand for efficiency and scale. But this is not a greenfield market.

Structural constraints - accuracy requirements, workflow inertia, data access, and the centrality of human judgment limit the pace and extent of change. At the same time, rapid advances in foundation models are compressing differentiation and eroding defensibility of many point solutions.

There is a role for third-party vendors, particularly those that can integrate deeply into workflows, unlock proprietary data, and meet institutional standards for governance and compliance. However, outcomes for these companies are likely to be more limited than current enthusiasm suggests.

Rather than a broad set of venture-scale winners, we expect a more concentrated market with a small number of durable platforms and a long tail of commoditized tools. We expect a number of these tools will likely be acquired by incumbents seeking to remain relevant such as FactSet, so we expect outcomes to be skewed towards modest exits rather than outsized returns.

AI will change how investments get done but from an investment perspective, this is a market defined by constraints, consolidation, and a small set of winners.

What would change our view? We are looking for startups that are reimagining – not just streamlining workflows. We think these workflows will be fundamentally rebuilt, creating opportunities both for vertical and horizontal platforms that will power the next generation of knowledge work. We are particularly interested in solutions that build on proprietary data and benefit from strong deep network effects.

We would love to hear from you - please reach out to chat to Julie McCrimlisk at jm@illuminatefinancial.com