Private Credit is Exploding: Is There Room for Venture Capital?

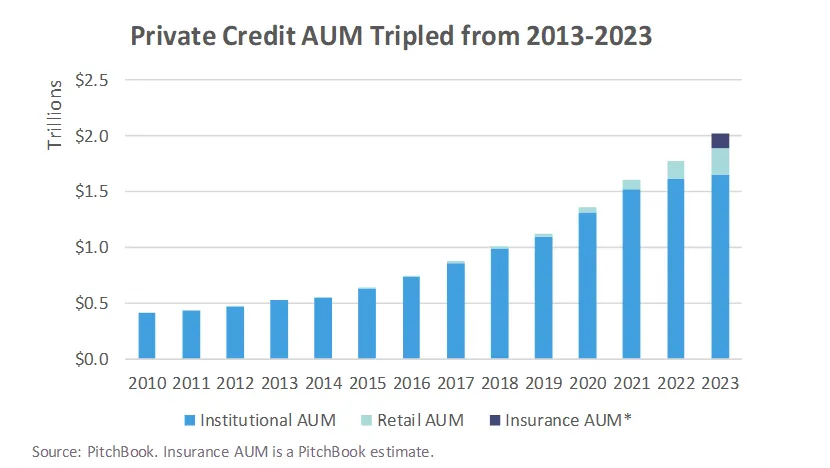

Private credit began to take off during the Great Financial Crisis as banks looked to de-leverage and PE shops began taking a more active role in direct lending. Fast forward to the 2020s and private credit AUM has more than tripled.

Private credit is exploding, but are there opportunities for venture-backed companies to capitalize on the private credit boom? In this post, we look at opportunities to invest across the private credit universe — from origination opportunities through infrastructure and workflow optimization.

The Evolution of Private Credit

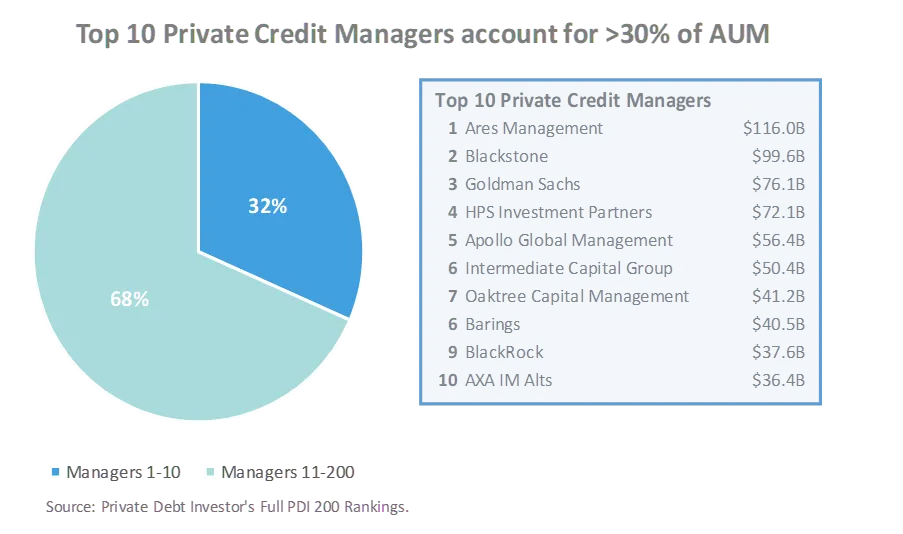

The private credit market more than tripled from 2013 to 2023 with Pitchbook estimates placing institutional AUM at $1.7T for 2023 and over $2T when including retail and insurance AUM. The market is consolidated with the top 10 private credit managers representing >$626B in private credit AUM or >30% of top 200 private credit managers’ AUM.

The growth in AUM has been accompanied by a flood of announcements as alternative asset managers and traditional lenders launch private credit initiatives and acquire private credit firms. Notable announcements include Jefferies launching a Direct Lending BDC anchored by the ADIA, Barclay’s partnership with AGL, Citi and Apollo’s $25B private credit/direct lending program, BNP and Apollo’s $5B ABF collaboration, Janus’ acquisition of Victory Park Capital, and Blackrock’s planned acquisition of HPS Partners.

While traditional lenders rush to partner with private credit funds, we are also seeing an increasing appetite to expand geographically and into new asset classes. Historically, direct lending opportunities in North America have accounted for the majority of private credit. However, we are increasingly seeing growth outside North America with Ares raising a €30B European direct lending fund and in asset-backed financing (“ABF”).

What’s Driving the Private Credit Arms Race?

Banks want to maximize ROE. Asset managers have cheaper access to capital since they are not subject to regulatory requirements. Many banks see this as an opportunity to partner with managers to offer ROE-accretive advisory services not subject to regulatory capital requirements. Partnerships also enable banks to offer customers a simpler loan process and loans to a broader customer base while cross-selling a broader suite of services provided by the bank. While many banks are taking this approach, a handful of banks including Goldman Sachs are going head-to-head with alternatives managers by raising private credit funds and JPMorgan is on the hunt to acquire a private credit firm.

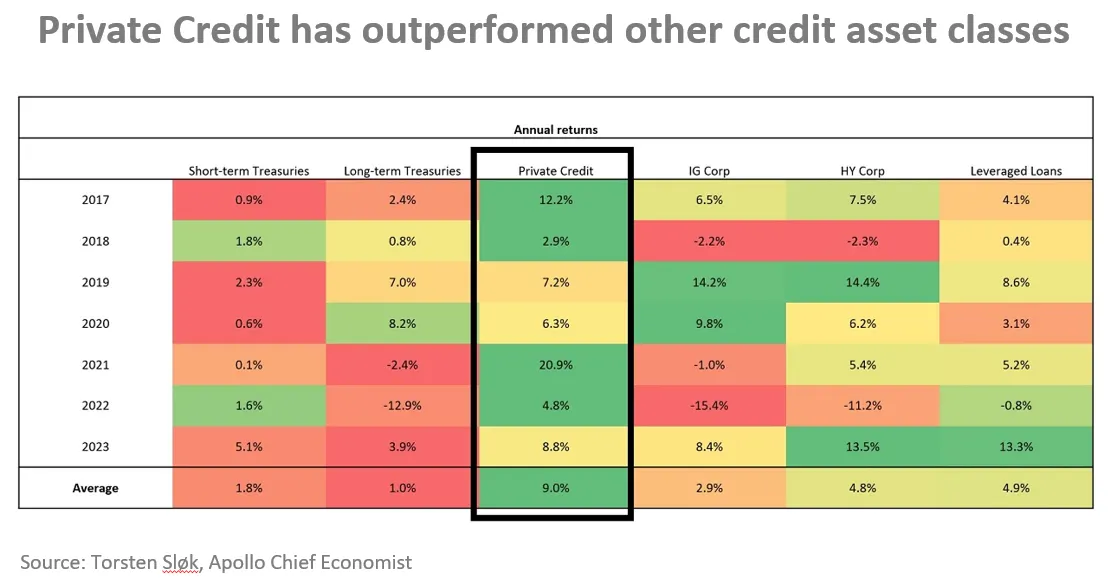

Investors want yield and diversification. Private credit offers higher yields than traditional fixed-income investments such as government bonds or investment-grade corporate bonds, as well as portfolio diversification given most investors are under-allocated to private credit. Private credit also offers attractive risk-adjusted returns for patient capital — pension funds, insurance companies, and sovereign wealth funds — who prefer longer-duration investment opportunities with steady, predictable cash flows.

Borrowers want better credit access. Private credit managers are less regulated so they can lend to a broader market and process loans faster than traditional banks. Direct lending — replacing traditional bank financing including offering loans to companies too small for the public market but too large for SMB bank loans — has dominated private credit activity to date. Private credit funds are also increasingly financing the ABF market as corporates look to offload balance sheet risk, for example, PayPal sold its BNPL book to KKR and Klarna sold its UK loan book to Elliott Advisors.

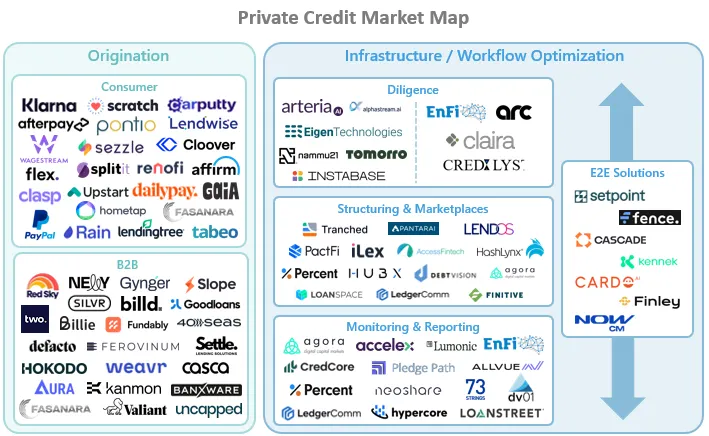

Two Ways to Play Private Credit: Origination Platforms and Infrastructure

We see two ways for VC investors to play the private credit boom: invest in origination engines or invest in infrastructure. Within origination, we see opportunities to build origination engines that expand existing product offerings, such as direct lending, or provide access to new product classes, such as equipment and supply chain financing. Within infrastructure, we see opportunities to improve efficiencies across the investment lifecycle with the biggest opportunities around data standardization, portfolio monitoring, and marketplaces.

Access is the Real Prize: Paying up for Origination Pipelines

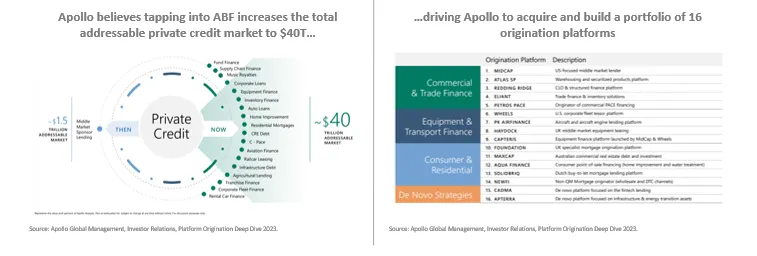

Direct lending accounts for the lion's share of private credit activity, but managers are increasingly looking to allocate to ABF as the direct lending market grows increasingly saturated. According to industry players, expanding to ABF will increase the addressable market to $20–40T depending on the asset classes included.

The principal challenge for managers looking to add “alternative” ABF products to portfolios is access. Challenges accessing high-volume and low-ticket size loans have led to recent deals where asset managers are buying loan books from fintechs including PayPal selling its BNPL book to KKR and Klarna selling its UK loan book to Elliott Advisors. This is just the tip of the market. Ultimately, we believe managers will continue to leverage third parties or acquire origination engines to bring sourcing capabilities in-house as they build diversified portfolios of ABS origination platforms.

As we previously wrote, we believe lending is a massive market and the next generation of successful lending startups will be verticalized lenders. While we expect most of these origination engines will exit to strategics or PE before becoming unicorns, we do see opportunities for venture-scale returns at an early-stage. We see the biggest opportunities on the ABF side. However, there are several drawbacks for venture investors:

- Early-stage startups often take balance sheet risk before achieving the necessary scale to graduate to a private debt facility and, eventually, a bank facility.

- Management teams often overlook the risk/growth trade-off as both volume growth and margin expansion inevitably involve increasing risk by moving down market.

Given the drawbacks to investing in early-stage origination businesses, we would prefer to focus on Series B+ businesses that have already demonstrated product market fit, have been able to offload some of the balance sheet risk, and have been able to demonstrate disciplined growth without deteriorating lending metrics. However, given our belief that most companies will be taken out before they can achieve unicorn-scale, we do see more limited opportunities for venture scale returns at this stage. That being said, we do believe companies that can carve out a unique niche in the market are worth backing at an early stage and, in those unique circumstances, could generate significant returns.

Fixing the Foundation: Infrastructure and Workflow Optimization in Private Credit

Credit markets suffer from fragmented, unstandardized, unstructured data. Private markets lack established infrastructure and optimized workflows. These issues are not new. We’ve invested in companies looking to build infrastructure to automate workflows across financial services:

- We invested in Arteria to solve the issues underlying financial services contracts by enabling clients to transform free-form legal contracts into structured, actionable data.

- We invested in Accelex to focus on transforming unstructured private markets documents into actionable investment data and insights and offer portfolio management.

Private credit suffers from a combination of the credit market and private market pain points– pain from unstructured data to manual workflows to address legacy systems and customized reporting requirements. While we’ve invested in broader market solutions, we’ve had 30+ conversations across private credit and repeatedly hear it referred to as the “wild west.” We see opportunities to build solutions to address some of the pain points that have echoed through our conversations including:

- Data lifecycle management: While document analysis and data/covenant extraction has become standard for many documentation solutions, most solutions struggle to handle unstructured covenants. We see the ability to parse, monitor, and analyze unstructured covenants pre/post-investment as a game-changer since most incumbents struggle to handle unstructured covenants in post-investment workflows.

- Syndication / marketplace solutions: While syndication isn’t an acute pain point today given the direct lending dominance and limited number of large-scale players within private credit, there is no “liquid” market for private credit and no golden source of private credit market data. We see an opportunity to create a private credit marketplace that would provide private credit market data to better-enable participants to evaluate private credit instruments.

Private credit suffers from acute pain points, but the TAM for private credit-specific workflow solutions is small. The top 10 private credit managers account for >30% of private credit AUM. Selling SaaS solutions to private credit heavy-weights limits the market size since most players are building custom solutions in-house and only a handful have deep enough pockets to pay 1M+ per year.

As we previously wrote, we believe lending is a massive market and the next generation of successful lending startups will be verticalized lenders. While we expect most of these origination engines will exit to strategics or PE before becoming unicorns, we do see opportunities for venture-scale returns at an early-stage. We see the biggest opportunities on the ABF side. However, there are several drawbacks for venture investors:

- Early-stage startups often take balance sheet risk before achieving the necessary scale to graduate to a private debt facility and, eventually, a bank facility.

- Management teams often overlook the risk/growth trade-off as both volume growth and margin expansion inevitably involve increasing risk by moving down market.

Given the drawbacks to investing in early-stage origination businesses, we would prefer to focus on Series B+ businesses that have already demonstrated product market fit, have been able to offload some of the balance sheet risk, and have been able to demonstrate disciplined growth without deteriorating lending metrics. However, given our belief that most companies will be taken out before they can achieve unicorn-scale, we do see more limited opportunities for venture scale returns at this stage. That being said, we do believe companies that can carve out a unique niche in the market are worth backing at an early stage and, in those unique circumstances, could generate significant returns.

Fixing the Foundation: Infrastructure and Workflow Optimization in Private Credit

Credit markets suffer from fragmented, unstandardized, unstructured data. Private markets lack established infrastructure and optimized workflows. These issues are not new. We’ve invested in companies looking to build infrastructure to automate workflows across financial services:

- We invested in Arteria to solve the issues underlying financial services contracts by enabling clients to transform free-form legal contracts into structured, actionable data.

- We invested in Accelex to focus on transforming unstructured private markets documents into actionable investment data and insights and offer portfolio management.

Private credit suffers from a combination of the credit market and private market pain points– pain from unstructured data to manual workflows to address legacy systems and customized reporting requirements. While we’ve invested in broader market solutions, we’ve had 30+ conversations across private credit and repeatedly hear it referred to as the “wild west.” We see opportunities to build solutions to address some of the pain points that have echoed through our conversations including:

- Data lifecycle management: While document analysis and data/covenant extraction has become standard for many documentation solutions, most solutions struggle to handle unstructured covenants. We see the ability to parse, monitor, and analyze unstructured covenants pre/post-investment as a game-changer since most incumbents struggle to handle unstructured covenants in post-investment workflows.

- Syndication / marketplace solutions: While syndication isn’t an acute pain point today given the direct lending dominance and limited number of large-scale players within private credit, there is no “liquid” market for private credit and no golden source of private credit market data. We see an opportunity to create a private credit marketplace that would provide private credit market data to better-enable participants to evaluate private credit instruments.

Private credit suffers from acute pain points, but the TAM for private credit-specific workflow solutions is small. The top 10 private credit managers account for >30% of private credit AUM. Selling SaaS solutions to private credit heavy-weights limits the market size since most players are building custom solutions in-house and only a handful have deep enough pockets to pay 1M+ per year.

Press enter or click to view image in full size