Planning a fundraise — it always takes longer than you think

A sometimes-surprising reality of being a founder is that fundraising can become your full-time job. Although every process and business will have its differences, the more you can plan and prepare, the smoother it will inevitably be. Here are a few suggestions of how you could think about approaching a Seed/Series A fundraise.

Know the labels and metrics

According to Crunchbase, only 42% of Seed-funded startups go on to raise a Series A round. What a ‘Series A’ label means has also been changing, with more companies splitting early funding into multiple rounds (early seed, late seed, seed extension, pre-A, early A…).

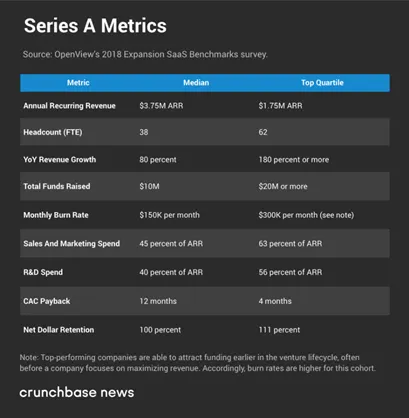

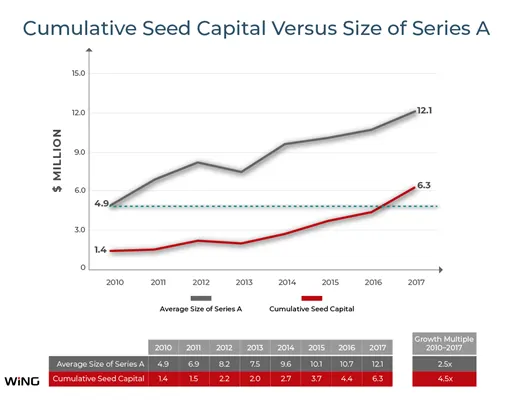

In the minds of most founders, a Series A is the first non-friends and family round. In the minds of most investors however, a Series A is growth funding for a company that has a commercially viable product, usually demonstrated through a c$1m+ ARR. The amount raised varies enormously depending on the rate of growth, size of opportunity, revenue profile and region, as you can see from the tables collated by OpenView and Wing VC (published in TechCrunch).

In Europe specifically, Index Ventures have stated that they view a c$5m round as the typical ‘Series A’ size but in a wide $3-$20m range. The general trend we are seeing, is for businesses to raise more cumulative finance at the Seed stage, with bigger Series A rounds completed later.

Where does your business fit?

With these labels in mind, stand-out founders will understand the stage of their business and how to position themselves to investors.

To justify raising any amount of money, you will need to have a clear and reasonable plan on how you will spend it, and the key milestones to reach. Once you know how much funding you will need to get to the next stage, then compare this to the figures above to understand the kind of investors that will be most suitable. If you are still in the early stages of revenue generation, with positive but not marked growth rates, then a Seed/Late Seed fund is probably the best fit. In contrast, if you have started to hit your stride with decent growth rates and have clients coming on quickly, then investors will be more receptive to a ‘Series A’ budget and plan.

As a rule of thumb, we try and make sure that companies have about 18mths runway after a raise as this gives the team enough breathing room between financings to get on with running and building the business. Therefore think about how much runway you are working into your budgets in a conservative scenario so you can be realistic about how much cash the business needs. Just don’t forget to sense check it against revenues!

Prioritise your investors

Good founders should think of investors in the same way they think of hiring key employees and ask questions like who has the best experience for the job and fits culturally. Before targeting specific funds, think about what you would like an investor to bring to the table other than money. It might be their domain expertise, networks, brand, support, governance, the PR… like candidates for any role, each investor is different and has pros and cons.

The reason it’s important to think more holistically about the value an investor can bring at the outset is because it’s easy to weigh one metric alone — the valuation being offered — once you are in the process. While this is certainly a huge consideration, in the same way you would not hire the ‘cheapest’ employee for a key role, it also follows that the ‘best priced’ investor might not offer the best value in the long-term.

Once you know what you want from an ideal investor, a good way to start building a list of targets is to look online at the ‘CVs’ of funds; their portfolio companies and investment thesis. This information should not be hard to find as most funds will have websites, blogs etc sharing this.

Not only will this give you a sense of the kind of companies the fund has invested in (indicating whether you would be a fit for them), it helps you answer the question “will they be the right investor for you?”

How long will it take?

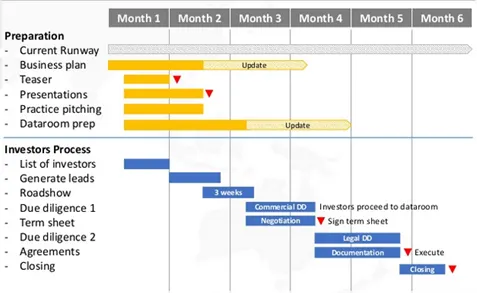

Once you have thought about the shape of your round and ideal investors, the hardest part begins. While things will be easier if you have a targeted list and focused view of what you are looking for, you will need to have a lot (think c30–50 investors for a seed round) of meetings before getting to a term sheet.

From what we have seen, it takes at least 4–6 months on average to run a fundraising process from start to finish. Getting to a headline agreement and term sheet with a lead investor is also only one step. It’s likely to take a minimum of 4–6 weeks to close out legal documentation after this. Given the time it will take to close, it’s important to plan so you are not facing a cash crunch in the middle of the negotiations. This is definitely not a position you, or your new investor for that matter, would want you to end up in!

No fundraise will ever run entirely to script, but we have seen that founders who plan ahead and approach the process in a considered way are able to get to an answer faster, and find the investors best aligned with their businesses.